The financial landscape has undergone a significant transformation in recent years, primarily driven by technological advancements and changing consumer preferences. Digital wallets, which allow users to store payment information and make transactions electronically, have emerged as a formidable alternative to traditional banking methods. Traditional banking, characterized by physical branches, paper-based transactions, and face-to-face interactions, has been the cornerstone of financial services for centuries.

However, the rise of digital wallets has prompted a reevaluation of how individuals manage their finances, make purchases, and interact with financial institutions. Digital wallets, such as PayPal, Apple Pay, and Google Wallet, offer a seamless way to conduct transactions without the need for cash or physical cards. They leverage mobile technology to provide users with a convenient platform for payments, bill splitting, and even loyalty rewards.

In contrast, traditional banking relies on established systems that often involve lengthy processes for account management and transaction execution. As consumers increasingly seek efficiency and convenience in their financial dealings, the competition between digital wallets and traditional banking is intensifying, leading to a dynamic evolution in how financial services are delivered.

Security and Fraud Protection

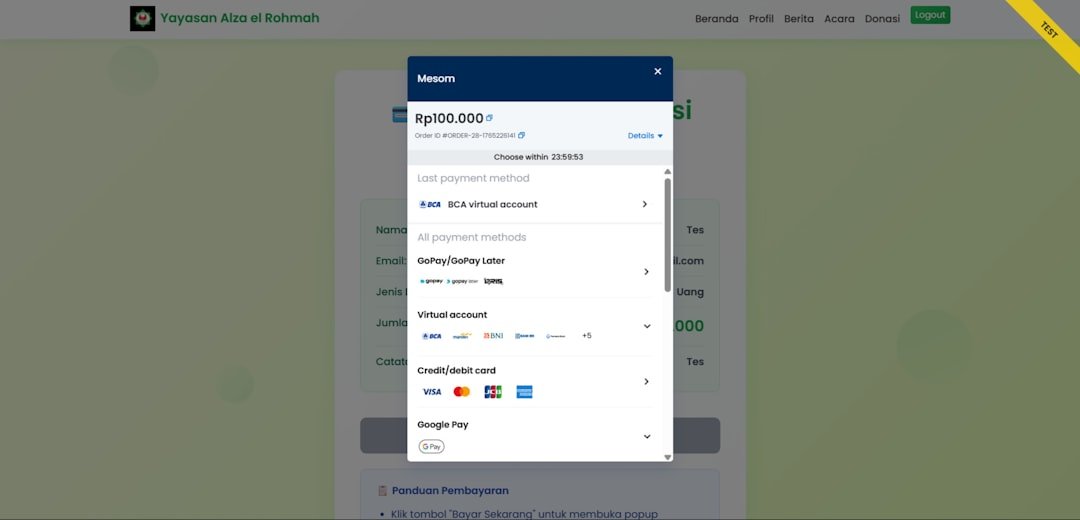

When it comes to financial transactions, security is paramount. Digital wallets employ a variety of security measures to protect users from fraud and unauthorized access. For instance, many digital wallets utilize encryption technology to safeguard sensitive information such as credit card numbers and personal identification details.

Additionally, biometric authentication methods like fingerprint scanning or facial recognition have become commonplace in digital wallets, adding an extra layer of security that is often absent in traditional banking systems. On the other hand, traditional banks have long established protocols for fraud detection and prevention. They typically monitor transactions for unusual activity and may alert customers if suspicious behavior is detected.

However, the reliance on physical cards can expose users to risks such as card skimming or theft. While both digital wallets and traditional banking systems have their strengths and weaknesses in terms of security, the rapid evolution of technology means that digital wallets are continually enhancing their protective measures to stay ahead of potential threats.

Convenience and Accessibility

One of the most compelling advantages of digital wallets is their unparalleled convenience. Users can make payments with just a few taps on their smartphones, eliminating the need to carry cash or search for a physical card. This ease of use is particularly beneficial in today’s fast-paced world, where time is often of the essence.

Digital wallets also allow for quick access to transaction history, making it easier for users to track their spending habits and manage their finances on the go. In contrast, traditional banking often requires customers to visit physical branches for certain transactions or services. While many banks have developed online platforms and mobile apps to facilitate remote banking, there are still limitations that can hinder accessibility.

For example, not all banking services are available online, and some transactions may require in-person verification. This can be particularly challenging for individuals living in rural areas or those with mobility issues. The convenience offered by digital wallets positions them as a more accessible option for a broader range of consumers.

Transaction Speed and Efficiency

The speed at which transactions are processed is another critical factor that distinguishes digital wallets from traditional banking methods. Digital wallets enable near-instantaneous transactions, allowing users to send money to friends or make purchases at retail locations without delay. This immediacy is particularly advantageous in situations where time-sensitive payments are required, such as splitting a bill at dinner or making an urgent online purchase.

Traditional banking methods often involve longer processing times due to the need for manual verification and approval processes. For instance, transferring funds between bank accounts can take several business days, especially if the transaction involves different financial institutions. This lag can be frustrating for consumers who expect quick resolutions to their financial needs.

As digital wallets continue to streamline transaction processes through advanced technology, they are setting new standards for efficiency in the financial sector.

Fees and Costs

| Feature | Digital Wallets | Traditional Banking |

|---|---|---|

| Accessibility | Available 24/7 via smartphone or web | Limited to branch hours and ATM availability |

| Transaction Speed | Instant or near-instant transfers | Typically 1-3 business days for transfers |

| Fees | Low or no fees for most transactions | Varies; may include maintenance, transfer, and overdraft fees |

| Security | Encrypted, multi-factor authentication, biometric options | Regulated with FDIC insurance and strong security protocols |

| Payment Methods Supported | Credit/debit cards, bank accounts, cryptocurrencies (varies) | Bank accounts, checks, credit/debit cards |

| Physical Presence | None; fully digital | Branches and ATMs available |

| Customer Support | Online chat, email, phone support (varies by provider) | In-person, phone, and online support |

| Use Cases | Peer-to-peer payments, online shopping, contactless payments | Deposits, loans, mortgages, savings, investments |

When evaluating the cost-effectiveness of digital wallets versus traditional banking, it is essential to consider the various fees associated with each option. Digital wallets often tout lower transaction fees compared to traditional banks. For example, many digital wallet providers charge minimal fees for peer-to-peer transfers or online purchases, making them an attractive choice for cost-conscious consumers.

Additionally, some digital wallets offer free services for basic transactions, further enhancing their appeal. Conversely, traditional banks may impose various fees that can accumulate over time. These can include monthly maintenance fees, overdraft charges, and transaction fees for wire transfers or international payments.

While some banks offer fee waivers based on account balances or customer loyalty programs, others may not be as flexible. As consumers become more aware of these costs, many are gravitating toward digital wallets as a more economical alternative for managing their finances.

Integration with Other Financial Services

The ability to integrate with other financial services is a significant advantage that digital wallets hold over traditional banking systems. Many digital wallet platforms offer features that allow users to link their accounts with various financial services such as budgeting tools, investment platforms, and cryptocurrency exchanges. This integration creates a holistic financial ecosystem where users can manage all aspects of their finances from a single application.

Traditional banks have historically been slower to adopt such integrations due to legacy systems and regulatory constraints. While some banks are beginning to offer similar functionalities through partnerships with fintech companies or by developing their own apps, they often lag behind the agility of digital wallet providers. As consumers increasingly seek comprehensive solutions that encompass all their financial needs, the ability of digital wallets to seamlessly connect with other services positions them as a more attractive option in the marketplace.

Customer Service and Support

Customer service plays a crucial role in the overall experience of using financial services. Digital wallet providers often rely on online support channels such as chatbots, email support, and extensive FAQs to assist users with their inquiries. While this approach can be efficient for straightforward questions or issues, it may lack the personal touch that some customers prefer when dealing with financial matters.

In contrast, traditional banks typically offer multiple avenues for customer support, including in-person assistance at branches and dedicated phone lines for customer service representatives. This face-to-face interaction can foster trust and provide reassurance during complex transactions or when resolving disputes. However, long wait times or limited availability can detract from the overall customer experience at traditional banks.

As both sectors continue to evolve, finding the right balance between technology-driven support and personalized service will be essential in meeting customer expectations.

Future Trends and Developments in Digital Wallets and Traditional Banking

The future of digital wallets and traditional banking is poised for further evolution as technology continues to advance at an unprecedented pace. One notable trend is the increasing adoption of blockchain technology within digital wallets. Blockchain offers enhanced security features and transparency that could revolutionize how transactions are recorded and verified.

As more consumers become comfortable with cryptocurrencies and decentralized finance (DeFi), digital wallets may expand their offerings to include these emerging financial products. Moreover, artificial intelligence (AI) is expected to play a significant role in shaping customer experiences across both digital wallets and traditional banks. AI-driven analytics can provide personalized recommendations based on spending habits or financial goals, enhancing user engagement and satisfaction.

Traditional banks may also leverage AI to streamline operations and improve fraud detection capabilities. As regulatory frameworks evolve to accommodate the growing influence of digital wallets, traditional banks may need to adapt their strategies to remain competitive. This could involve forming partnerships with fintech companies or investing in technology upgrades to enhance their service offerings.

The interplay between innovation and regulation will be crucial in determining how both sectors navigate the future landscape of financial services. In conclusion, the competition between digital wallets and traditional banking is reshaping how consumers interact with their finances. As both options continue to evolve in response to consumer demands and technological advancements, understanding their respective strengths and weaknesses will be essential for individuals seeking the best solutions for their financial needs.

FAQs

What is a digital wallet?

A digital wallet is an electronic device or online service that allows individuals to make electronic transactions. It can store payment information, passwords, and other personal data securely, enabling users to pay for goods and services digitally.

How do digital wallets differ from traditional banking?

Digital wallets primarily focus on facilitating quick and convenient digital payments and storing payment credentials, whereas traditional banking offers a broader range of financial services including savings and checking accounts, loans, and investment products.

Are digital wallets safe to use?

Yes, digital wallets use encryption and tokenization to protect users’ financial information. Many also require biometric authentication or passwords. However, users should ensure they use reputable digital wallet providers and maintain strong security practices.

Can digital wallets replace traditional bank accounts?

Digital wallets can complement but generally do not fully replace traditional bank accounts. While they facilitate payments and money transfers, they often lack features like interest-bearing accounts, loans, and comprehensive financial management services.

Do digital wallets charge fees?

Some digital wallets may charge fees for certain transactions, such as instant transfers or currency conversions, but many offer free basic services. Fee structures vary by provider.

Are digital wallets widely accepted?

Acceptance of digital wallets is growing globally, especially for online and contactless payments. However, acceptance can vary by region, merchant, and payment network.

How do I add money to a digital wallet?

Users can add money to digital wallets by linking them to a bank account, credit or debit card, or by receiving funds from other users. Some wallets also allow cash top-ups at participating locations.

Can I use a digital wallet without a smartphone?

Most digital wallets require a smartphone or compatible device to operate. However, some offer web-based access or physical cards linked to the wallet for in-person payments.

Is it easy to switch between digital wallets and traditional banking?

Yes, many digital wallets are designed to integrate with traditional bank accounts, allowing users to transfer funds between the two easily. However, the ease of switching depends on the specific services and providers involved.

What are the benefits of using digital wallets over traditional banking?

Digital wallets offer faster transactions, convenience for online and contactless payments, reduced need to carry physical cards or cash, and often enhanced security features like tokenization and biometric authentication.